Inheritance planning can be complicated, and one of the most common questions that we are asked is whether beneficiaries are required to pay taxes on what they inherit. The answer depends on several factors, including the type of asset inherited, federal tax rules, and the state where the deceased lived or owned property. Here's a comprehensive look at what you need to know.

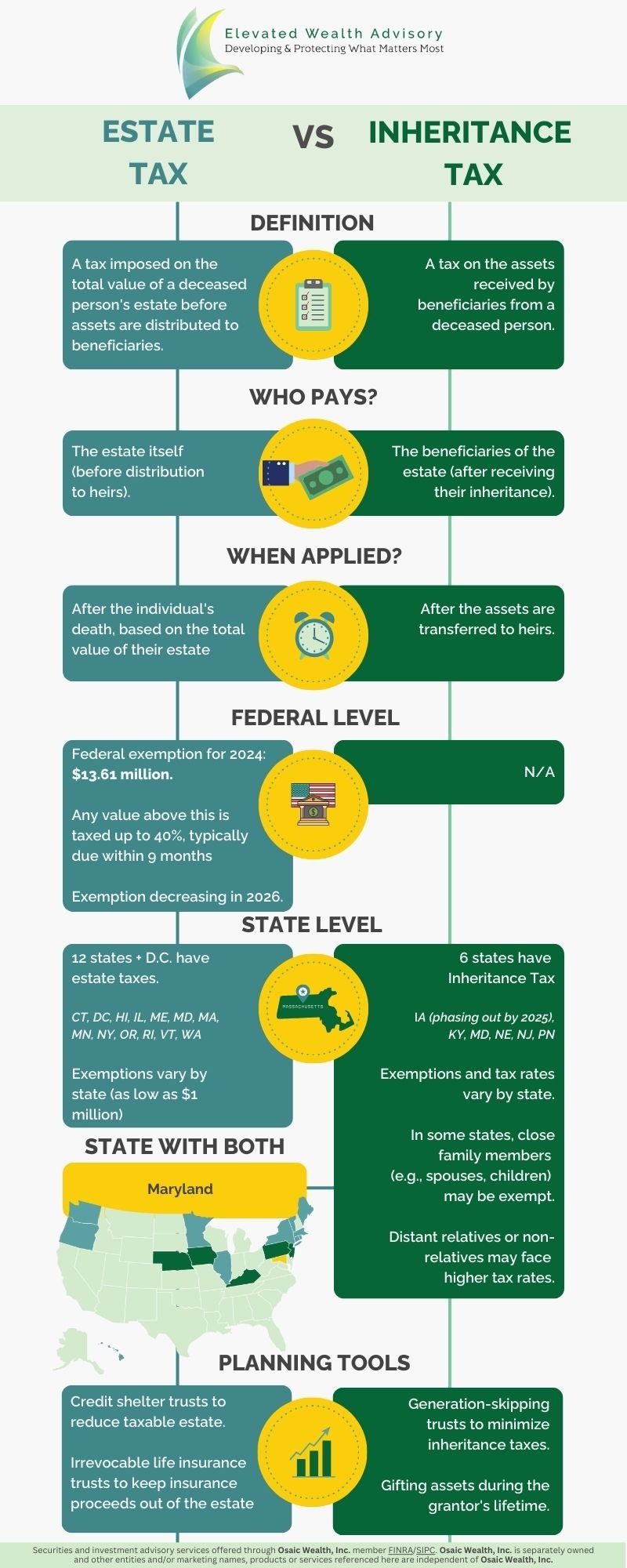

Understanding Inheritance Taxes vs. Estate Taxes

Before diving into specific tax rules, it’s essential to understand the difference between inheritance and estate taxes. These terms are often used interchangeably, but they refer to different types of taxes:

Inheritance Tax: Paid by the beneficiaries who receive assets from the estate. Not all states impose this tax.

Estate Tax: Levied on the deceased person’s estate before any assets are distributed to beneficiaries. The federal government and some states have estate taxes.

Federal Estate and Inheritance Tax

The good news for most beneficiaries is that the federal government does not impose an inheritance tax. This means that, generally speaking, beneficiaries won’t owe federal taxes on inherited assets.

However, federal estate taxes may apply to high-value estates. In 2024, the federal estate tax exemption is $13.61 million per individual. Estates below this threshold are not subject to federal estate taxes. For amounts exceeding the exemption, the tax rate can be as high as 40%. Importantly, this exemption is scheduled to decrease in 2026*, which makes long-term planning crucial.

*This is based on current tax laws sunsetting at the end of 2025. This is a key issue for the Trump Administration and is subject to change before the laws expire.

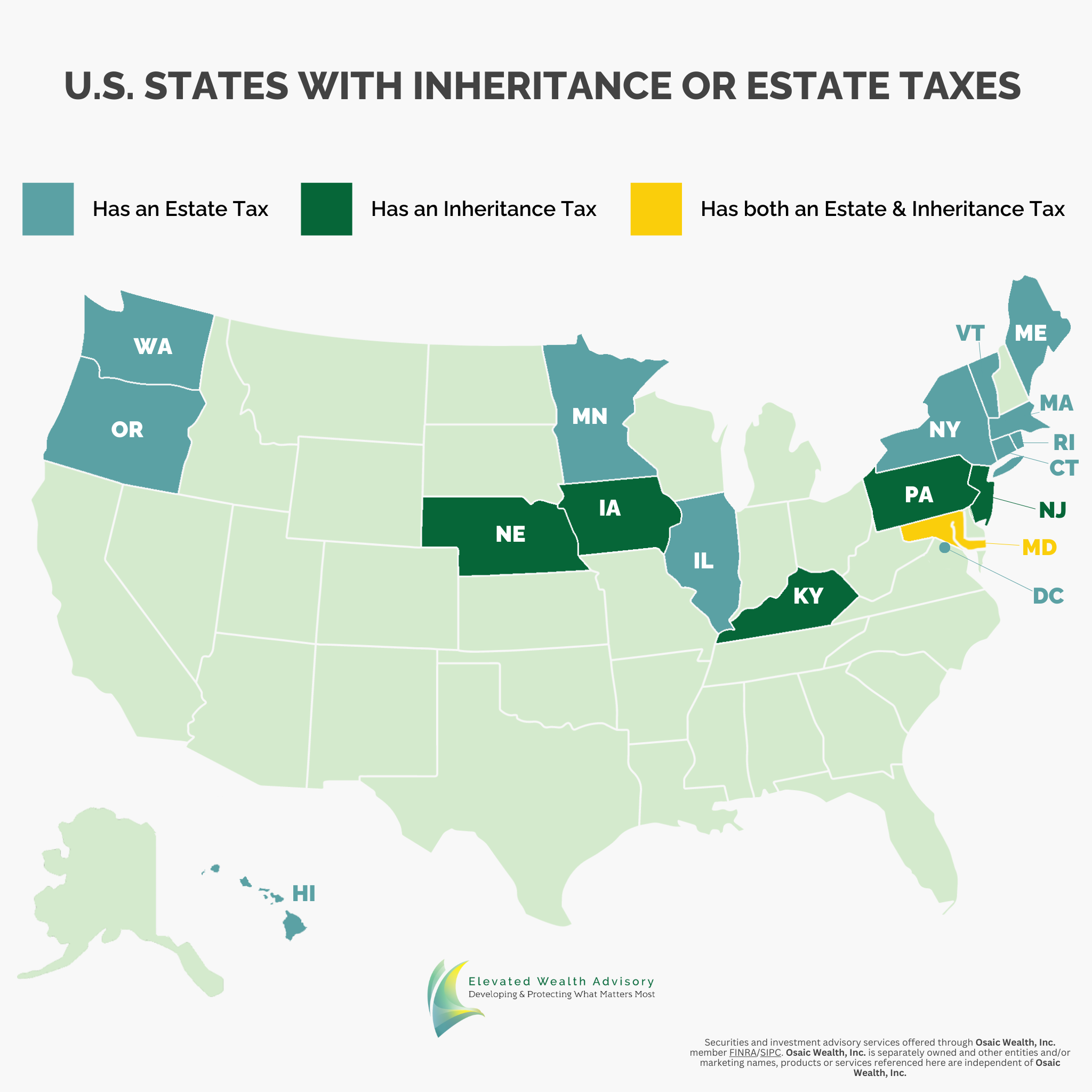

State Specific Estate Tax

Some states in the US impose their own estate tax. State estate tax exemption amounts vary significantly, with some states taxing estates valued as low as $1 million. Some states even have an estate tax for a surviving spouse, which you do not see at a federal level.

As of 2024, the following 12 states and the District of Columbia impose an estate tax:

- Connecticut

- District of Columbia

- Hawaii

- Illinois

- Maine

- Maryland

- Massachusetts

- Minnesota

- New York

- Oregon

- Rhode Island

- Vermont

- Washington

Some states, like Massachusetts and Oregon, have cliff taxes, meaning that if an estate exceeds the exemption by even $1, the entire estate is subject to taxation.Given these variations, high-net-worth individuals should incorporate estate tax planning into their financial strategy to minimize tax burdens.

1 https://www.irs.gov/businesses/small-businesses-self-employed/

2 https://taxfoundation.org/data/all/state/estate-inheritance-taxes/

State Inheritance Taxes

While there is no federal inheritance tax, some states impose their own inheritance taxes. As of now, the only states with inheritance taxes are:

Iowa (phasing out by 2025)

- Kentucky

- Maryland

- Nebraska

- New Jersey

Each state sets its own rules regarding exemption limits and tax rates, and it is the beneficiary, not the estate, who pays the inheritance tax. It’s important to consult with an advisor to understand the specific rules if the deceased had ties to one of these states.

Maryland is unique in that it has both a state estate tax and an inheritance tax.

3 https://taxfoundation.org/data/all/state/estate-inheritance-taxes/

Taxes on Inherited Retirement Accounts

If you inherit a retirement account, such as a traditional IRA or 401(k), the tax rules differ from other types of inheritance. Pre-tax retirement accounts follow specific distribution rules:

Non-Eligible Beneficiaries are required to fully deplete the inherited account within 10 years of the original owner’s death. This can create significant tax consequences, as distributions are considered taxable income.

If the original owner was already taking Required Minimum Distributions (RMDs), the person who inherited the account must take RMDs over the 10 years starting in 2025.

Eligible Beneficiaries typically have more flexibility and could roll the account into their own retirement plan, and not be subject to RMDs. Eligible Beneficiaries include:

- The deceased person's surviving spouse

- The deceased person's minor child

- A disabled person

- A chronically ill person

- A person who is no more than 10 years younger than the deceased person

- Trusts, estates, and charities

It’s highly recommended to consult with a financial planner or tax professional to understand the best strategy for managing inherited retirement accounts as there are specific rules for Eligible Beneficiaries. A spouse who inherited an IRA is going to have different options than a brother who is less than 10 years younger than his deceased sister will.

To help guide you through the options you may have, please see the flowchart below when it comes to an IRA you have inherited.

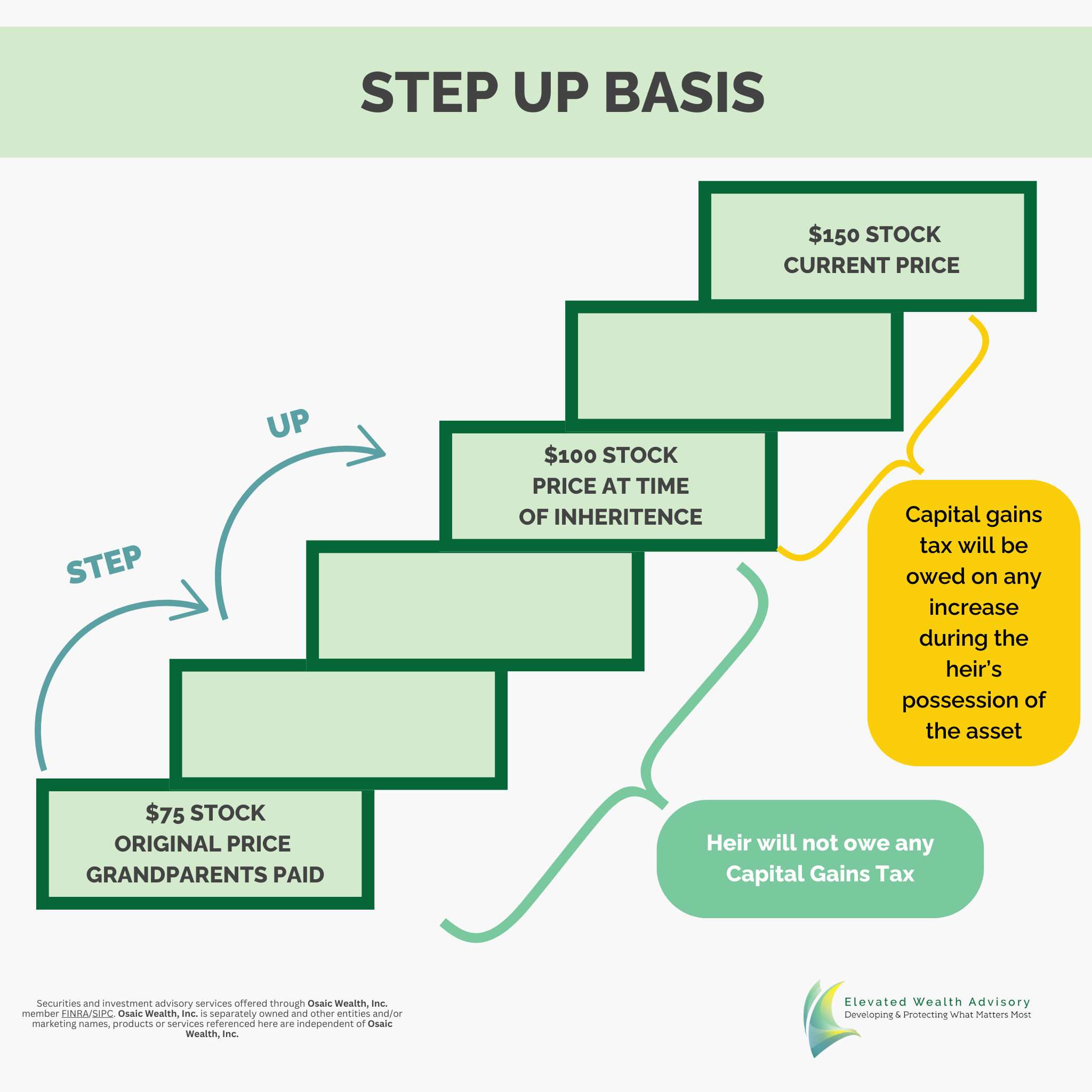

Step-Up in Basis for Inherited Taxable Assets

One tax benefit that beneficiaries often receive is the step-up in cost basis for inherited taxable assets. This applies to taxable investment accounts, real estate, and other taxable investments.

Here’s how it works:

- If the deceased originally purchased a stock for $25, and it was worth $100 at the time of their death, the beneficiary receives the asset at the $100 value. If they sell the stock for $110, they only owe capital gains taxes on the $10 increase.

This rule can significantly reduce the tax burden on beneficiaries. However, if the asset is gifted during the original owner’s lifetime, the beneficiary inherits the original cost basis, potentially increasing their capital gains tax liability.

Life Insurance Proceeds

Life insurance payouts are typically not subject to income tax for beneficiaries. However, if the policy was owned by the deceased and is part of their estate, it could be subject to estate taxes if the total estate value exceeds the federal or state exemption limits.

Inheritance Planning Tips to Minimize Taxes

To help beneficiaries avoid unnecessary tax burdens, consider the following strategies:

Trusts: Establishing trusts, such as irrevocable life insurance trusts (ILITs) or generation-skipping trusts, can help minimize tax liabilities.

Beneficiary Designations: Ensure that retirement accounts and life insurance policies have up-to-date beneficiary designations to avoid probate and potential tax implications.

Gifting: Lifetime gifting can reduce the size of an estate, potentially lowering estate taxes.

Final Thoughts

While beneficiaries generally don’t have to worry about federal inheritance taxes, understanding state tax rules and the implications of inheriting different types of assets is essential. Proper inheritance planning, including the use of trusts and strategic beneficiary designations, can help preserve your wealth and ensure it passes smoothly to your loved ones. Working with a financial planner, tax professional, and estate attorney can provide peace of mind and ensure that your family’s inheritance is handled efficiently and tax-effectively.