Inheritance planning can be complex, especially for grandparents who want to leave a meaningful legacy for their grandchildren. Proper planning ensures that your hard-earned wealth passes smoothly to the future generation while minimizing taxes and legal headaches. Here’s a guide to help you navigate the essential aspects of inheritance planning, including trusts, estate taxes, and the often-overlooked widow’s penalty.

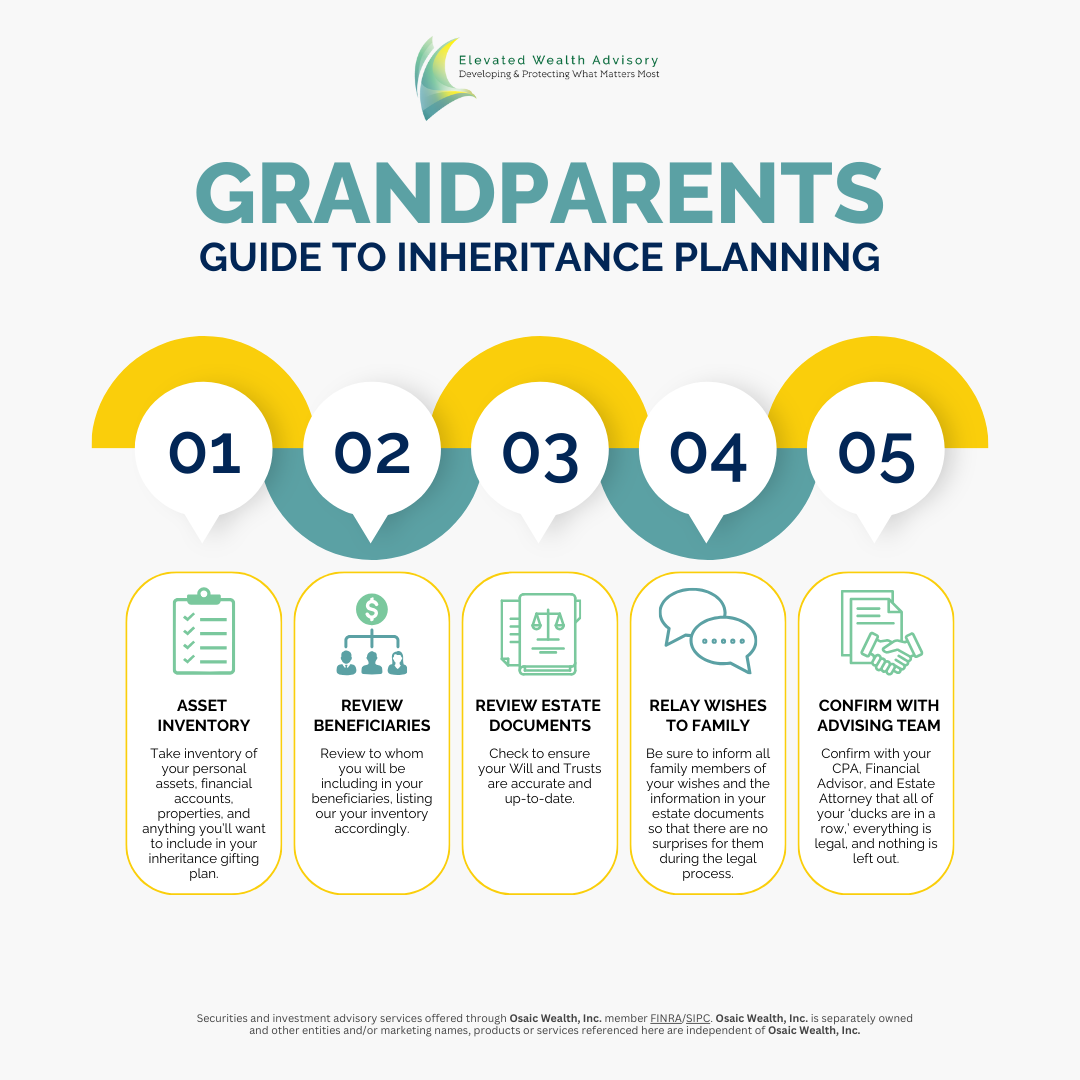

Where to Start for Inheritance Planning?

When we help Families with Family & Generational Planning, we start by listing and taking inventory of your assets and who you'd like to pass them down to. Double-check that your will and trusts are accurate and up-to-date. If you don't already have these in place, this is an essential piece of your inheritance gifting plan. Once everything is laid out the way you like, it's vital to relay these wishes to your family. This can sometimes be a tough conversation, however, it ensures there are no surprises during the legal process. Lastly, you'll want to confirm with your CPA, Financial Advisor, and your Estate Attorney that everything is lined up properly, legalized, and nothing is left out.

Texas Inheritance Tax Planning

Do beneficiaries have to pay taxes on inheritance? In the U.S., the federal government does not impose an inheritance tax, meaning your beneficiaries generally won’t have to pay taxes on what they inherit. However, some states levy their own inheritance taxes. Fortunately, Texas does not have an inheritance tax, making it a more favorable state for estate planning. It is recommended that you speak with your advisor to see if there is an inheritance tax in your state.

Estate vs. Inheritance Tax: What’s the Difference?

Estate tax and inheritance tax are often confused but serve different purposes. Estate taxes are levied on the value of the deceased’s estate before any assets are distributed to the heirs, while inheritance taxes are charged to the recipients of the estate.

Currently, the federal estate tax exemption is set at $13.61 million per individual, which means estates valued below this amount are exempt from federal estate taxes. However, amounts above the exemption can be taxed at rates up to 40%. Importantly, this exemption is set to decrease in 2026, making it crucial to plan ahead. Any estate tax is due to the IRS within nine months of your passing.

Not only is there a federal estate tax, but some states have their own “state estate tax”. There are 12 states (and one district) that tax an estate at the state level: Connecticut, District of Columbia, Hawaii, Illinois, Maine, Massachusetts, Maryland, New York, Oregon, Minnesota, Rhode Island, Vermont, and Washington. Some of the state estate tax exemption limits are as low as $1 million. Much different than the federal level.

There is no estate tax in Texas, but if you own property or other assets in states with estate taxes, your heirs might still face tax obligations. Planning with trusts and other estate planning tools can help navigate these complex rules.

The only states with an inheritance tax are Iowa (phasing out in 2025), Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. An inheritance tax is levied on the value of an inheritance received by the beneficiary, and it is the beneficiary who pays it. Each state varies on the exemption limits for an inheritance tax, and Maryland is the only state that has both a state estate tax, and inheritance tax.

Tax on Inherited IRAs or Other Retirement Accounts

Pre-tax, or “qualified,” savings accounts follow a distinct set of rules when it comes to passing them on to specific beneficiaries. To address these nuances, we’ve created a dedicated blog that explains how these accounts are treated depending on the beneficiary. For the purpose of this blog, if you designate your grandchildren as beneficiaries of these accounts and they are 18 years or older, they are required to fully deplete the inherited account within 10 years. This could have major unintended tax consequences for your grandchildren. I strongly recommend reviewing our blog focused on the rules for inherited qualified accounts, particularly for non-spouse beneficiaries.

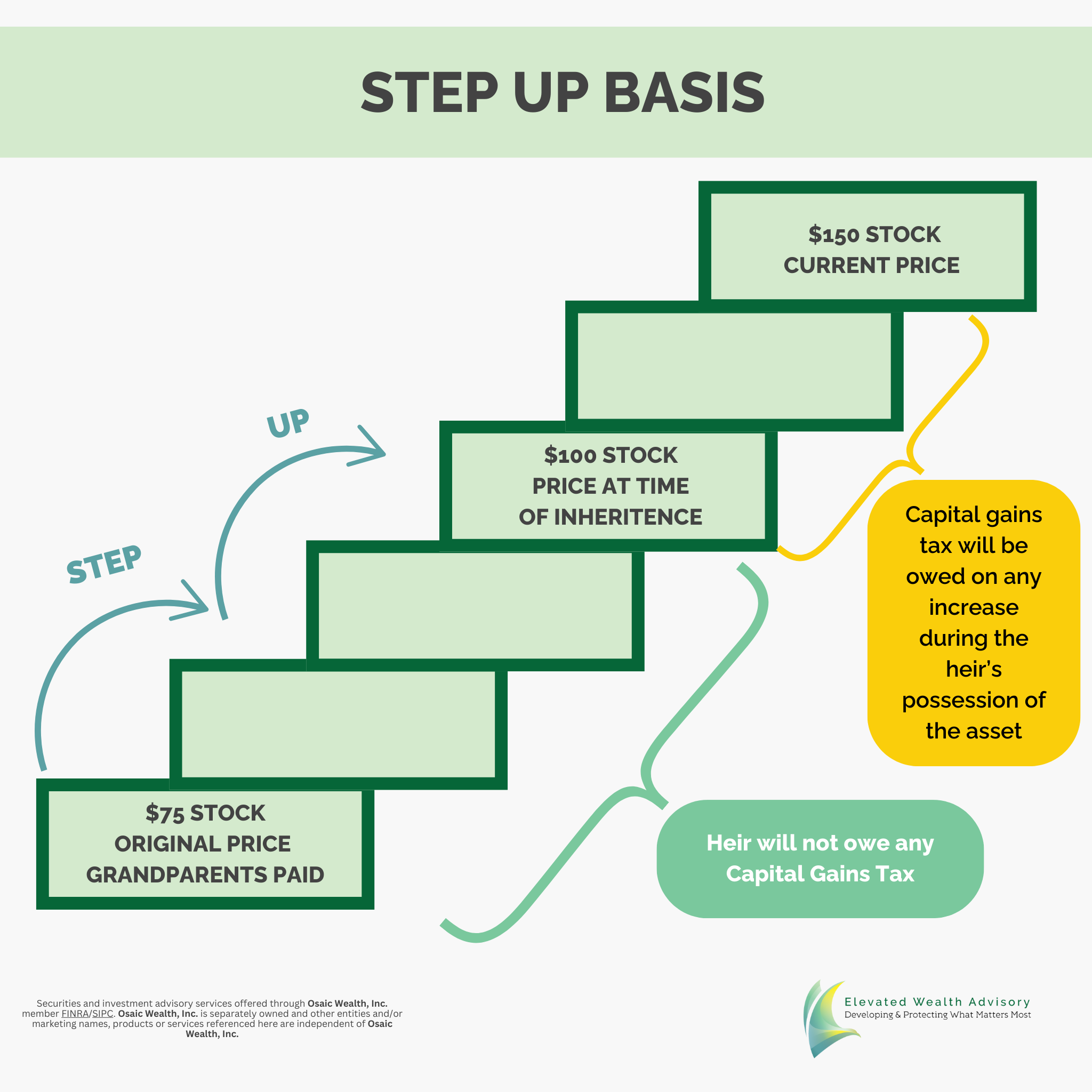

What is the “Step Up” Basis

Upon your death, any assets outside of a tax defered account (401k, IRA, etc.) will receive a “step up” in cost basis. For example, let’s say you originally bought a stock for $25, and when you passed away, it was worth $100. Your beneficiary will receive the stock at the value upon your passing, and doesn’t have to pay capital gains taxes on the $75 the stock has increased by.

However, beneficiaries might still face other tax implications if the stock further appreciates and they sell at a later date. To reduce the tax burden, it’s important to understand how these assets are taxed and consider options like “stepped-up basis,” which can minimize capital gains taxes.

Please keep in mind that the “step up” benefit is only for assets that are passed on after death. If an asset is “gifted” to a grandchild, they will receive the gift at the original cost basis, potentially increasing capital gains further.

Trusts for Grandchildren to Avoid Inheritance Tax

As with anything when it comes to estate planning, it depends on what your goals are. A simple revocable or irrevocable trust may be what you need. Or if you have a higher net worth, and want your dollars doing specific things when you pass, one of the following trusts may be for you. Remember the saying “Either trust your beneficiaries with your money, or have a trust so that you know what happens to your money.”

Generation-skipping trusts: Can allow trust assets to be distributed to non-spouse beneficiaries two or more generations younger than the donor without incurring GST tax.

Credit shelter trusts: Make full use of each spouse’s federal estate tax exclusion amount to benefit children or other beneficiaries by bypassing the surviving spouse’s estate.

Irrevocable life insurance trusts (ILITs): Purchase life insurance policies to provide immediate benefits upon death that do not usually pass through probate.

Each of the above trusts are considered advanced planning within the financial services industry, and it is highly recommended you work with a tax attorney, estate attorney, and financial advisor if you are looking to set these types of trusts up.

Inheritance Planning Options

Inheritance planning should not overlook other key elements, such as wills and the impact of retirement decisions. A will is a document that contains your direct wishes for your property and assets, as well as the care of your dependents. Failure to prepare a will typically leaves decisions about your estate in the hands of judges or state officials and may also cause family strife. Not having a will could make your loved ones pay legal fees because of the time it takes to settle your estate in court.

One aspect often overlooked in inheritance planning is the widow’s penalty. This penalty occurs when a surviving spouse moves into a higher tax bracket due to the loss of income splitting after their partner’s death. This can result in a significant increase in taxes during retirement, reducing the value of the inheritance left to your beneficiaries. Proper planning with trusts, beneficiary designations, and other tax strategies can help mitigate this penalty.

Is Inherited Money Taxable?

Like anything else with financial planning: it depends.

Effective inheritance planning involves more than just drafting a will. By understanding the complexities of tax consequences, setting up trusts, and having a clear plan for your hard-earned dollars, you can ensure that your legacy is preserved and passed on to your grandchildren in the most efficient way possible. Working with a financial planner who specializes in estate planning can provide peace of mind and help you make the best decisions for your family’s future.